Shenzhen Xino Business Consultant Ltd.

TEL: +86-755-25921519

Email: info@xino86.com

Add: 13F, Shangbu Bldg, Nanyuan Road, Futian, Shenzhen, GD, China

Taxation in China

Corporate Taxation Tax and Tax Rate

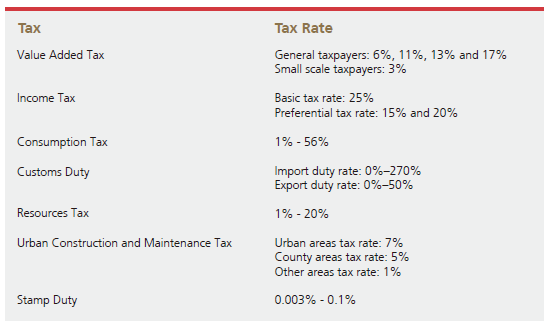

Taxes levied by China towards enterprises mainly include corporate value added tax, income tax, consumption tax and customs duty. China practices both territorial principle and personal principle on taxpayers, under which the tax resident enterprises shall pay corporate income tax on their profits made both at home and abroad. In addition, in order to avoid double taxation, China has signed Avoidance of Double Taxation Agreement with more than 100 countries and regions in the world. According to the agreement, the taxpayers of one party receive tax concessions in the other party of the agreement.

types-of-corporate-tax-and-tax-rates

Major Corporate Tax Incentives

- • Preferential income tax rate: 15% for high-tech enterprises, 20% for small and thin-profit enterprises, and 15% for government-sponsored industry in western regions.

- • Equipment procurement and investment for environmental protection, energy/water conservation and safety production may be deducted from the taxable income.

- • In addition to the stipulated deduction, an additional deduction of 50% of the R&D expenses may be conducted.

- • An enterprise may be free from corporate income tax if the income arising from transfer of technology is less than RMB5,000,000 in a year of assessment, and 50% corporate income tax will be collected on the portion except the RMB5,000,000 income.

- • In Special Economic Zones (Shenzhen, Zhuhai, Shantou, Xiamen and Hainan) and Pudong New District of Shanghai, high-tech enterprises are free from corporate income tax for the first two years, and pay 50% of the corporate income tax in the following three years, commencing as of the date of its first-time business revenue.

Individual Taxation Coverage

Any person shall pay individual income tax on the portion of his/her salary made and paid in the territory of China and by enterprises within the territory of China, no matter whether such salary is paid by the employer from the China or from abroad, as the source of income is China, thus, individual income tax is levied towards on such salary.

According to the Avoidance of Double Taxation Agreement signed between China and the home country of a foreigner, the foreigner concerned may not pay individual income tax in China in any of the following situations:

- • The foreigner is employed by a non-China-based company;

- • The foreigner has stayed in China for not more than 183 days within a year (from 1 January to 31 December);

- • The foreigner's salary is paid by an overseas company rather than a domestic company.

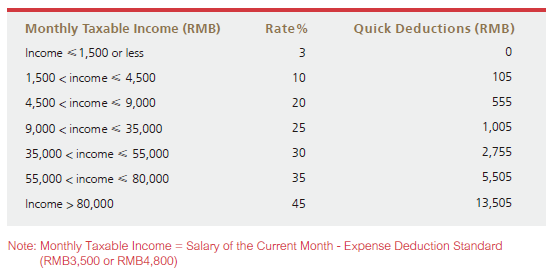

Tax Rate

The tax rate of individual income tax is 3% to 45%. Chinese residents and foreigners (including people from Hong Kong, Macau and Taiwan) shall pay individual income tax on the part of income exceeding RMB3,500 or RMB4,800 respectively.

Table of Individual Income Tax Rate